My commute to work takes me down Milwaukee Avenue through Logan Square and Wicker Park. If you haven't been there recently, that stretch is practically one long construction zone, in part due to new apartment-building construction. There's L, for instance, a mixed-use development with a 200-space bike room, a bike-maintenance station, and 120 units that start at $1,575 for a junior one-bedroom and go up to $3,900 for a three-bed. (When the transit-oriented development at 1611 West Division went up in 2013, its 99 apartments went for $1,495 to $3,295.) The Aldi at Milwaukee and Leavitt, next door to the 606, just came down for a 95-unit building due later this year. Logan Square's "twin towers" will add 213 units.

It's a lot of new apartments, and if neighborhood trends hold, they won't be cheap. So, who's renting these?

Lots of people, it turns out. DePaul's Institute of Housing Studies has a new report on Cook County's rental market, and there's been a dramatic change in recent years among its renters. Here are the top five groups, broken down by age and average median income (AMI), in terms of the raw number of renters. (For reference, Cook County's average median income in 2010-2014 is $54,828.)

Five Biggest Groups of Renters

| Renters, 2007 | Income Bracket | Renters, 2014 | Income Bracket |

|---|---|---|---|

| 42,525 | 25-34, 50-80% AMI | 54,434 | 25-34, 120-200% AMI |

| 39,424 | 25-34, 0-30% AMI | 51,434 | 25-34, 80-120% AMI |

| 39,086 | 45-54, 0-30% AMI | 50,460 | 25-34, 0-30% AMI |

| 36,289 | 25-34, 80-120% AMI | 49,584 | 25-34, 50-80% AMI |

| 34,482 | 35-44, 0-30% AMI | 43,013 | 35-44, 0-30% AMI |

Renters between the ages of 25-34, making between 120 and 200 percent of the area median income—$74,000 to $123,000 in 2014—are now the biggest demographic in the county rental market.

In 2007, that demographic didn't even make the top five; it consisted of 26,532 renters. That number more than doubled, adding an additional 27,902 middle/upper-middle class renters. Over the same period, renters making 200 percent or more of the area median income nearly doubled, rising from 10,809 in 2007 to 20,056.

And as the new developments suggest, many of those new renters are moving into relatively large apartment complexes.

.png)

The supply of units in buildings of five units or more increased by over 82,000 from 2007 to 2014. The increase in single-unit rentals also increased by more than 40,000. What stagnated? The classic Chicago two- and four-flats. Daniel Kay Hertz has written a great deal about this—how medium-density two- and four-flat rentals are being deconverted into luxury multi-unit buildings housing fewer people, or into expensive single-family homes:

But because Chicago’s zoning code fits so snugly over its neighborhoods outside of downtown – so snugly, in fact, that maximum allowed densities are frequently much lower than what already exists – builders have not been able to add much new housing. Instead, they maximize their profits by turning two-flats into luxury two-flats, or into mini-mansions for a single family. As a result, as places like Lincoln Park get more desirable than they’ve ever been, fewer people are able to live there, and its population remains about 40 percent below its peak, depriving the rest of the city of whole heaps of tax money that we might be able to spend on schools, roads, transit, and so on.

I watched this happen on my own block, when I lived on the border of Humboldt Park and Ukrainian Village; at one point, we had simultaneous deconversions from multi-unit buildings to single-family homes going on next door and two doors down. A third was happening kitty-corner to us on the next block. As Chris Hagan reported for WBEZ in March, West Town, Lake View, North Center, Lincoln Park, and Logan Square were vast outliers in terms of combined demolitions and new construction; it's enough that planners and politicians are concerned about how decreasing density could affect commercial activity in thriving, wealthy neighborhoods.

And Hagan echoed what Hertz wrote:

In addition to demand for access to good elementary schools, there are legal reasons behind the transformation from multi-unit buildings to single-family homes: There’s little to stop a developer or homeowner who wants to deconvert.

The Chicago zoning code allows developers to build single-family homes in any residential area, but adding units requires city approval. That increases costs and complexities for any developer wanting to add density.

It's not just zoning, though. There are more basic financial reasons why developers are inclined to build larger buildings and skip the two- and four-flats that have historically made up so much of the city's rental infrastructure.

"From the financial side, particularly for a rental two-to-four, it's not an easy financial thing to do … in terms of getting financing together, in terms of how you acquire the capital," says Geoff Smith, director of the Institute of Housing Studies. "The way it all shakes out is that it's far more efficient and far more profitable to do big deals or smaller deals. The two-to-four-unit buildings that are new development are mostly condos."

Like so much with housing, it goes back to the financial crisis, he explains.

"The default rates on two-to-four [flats] were much higher, because a vacancy on one of those units can be 25 percent, and if you're relying on that income to pay your mortgage, it makes it a much riskier proposition. During the financial crisis, and even still, the underwriting got much tighter on those types of properties," Smith says.

More difficult, expensive underwriting favors larger projects, but there are other financial incentives as well.

"When you get to the five-plus unit side of things, you're in the multi-family, more of a commercial-lending universe," Smith says. "And from a commercial-lending perspective, if you're making a loan under like three million dollars, it just becomes really expensive to underwrite, because it's the same price to underwrite a one-million-dollar loan as it is to underwrite a five-million-dollar loan, effectively, so lenders are just going to underwrite that five-million-dollar loan, because they get more fees from that. The servicing is more lucrative. So when you look at the lending trends, the financing is really going to these larger deals."

The financial crisis also reduced the number of lenders who were more inclined to finance lower-density rental projects.

"The smaller deals used to be under the auspices of community banks—the banks that had this local knowledge, and had that niche of the market really locked down," Smith says. "They were hit really hard by the financial crisis. Their portfolios were in tough shape; a lot of them went out of business, or were acquired. They got out of that game. To the extent that they're getting back into [mortgages], they're moving to the larger loans as well … It's just easier to do these bigger loans, and that tends to lend itself to bigger properties in higher-cost areas."

The direction Chicago's market has taken, towards high-density, high-rent buildings in or near the central city, is particularly relevant as the mayor's plan to expand high-density downtown zoning goes before City Council. The plan would leverage this trend, charging developers for the newly allowed density and directing that money into underserved neighborhoods.

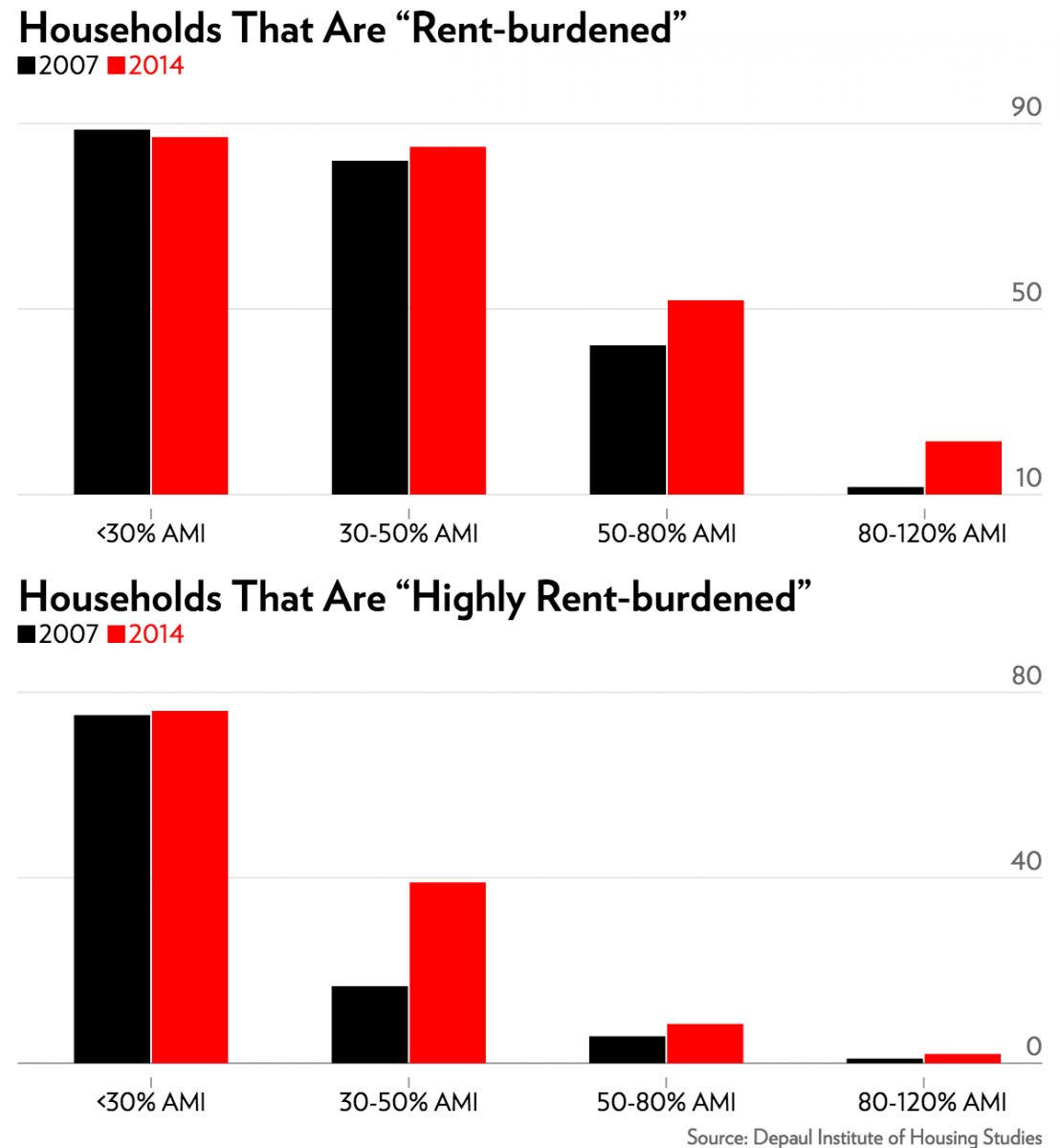

And there are plenty of neighborhoods that need the help. The other major trend in the IHS report is the increase in rent-burdened households—or households that spend at least 30 percent of their income on rent.

The percent of rent-burdened households in the very lowest income bracket—less than 30 percent of the area median income (or less than $16,448)—didn't change much, but it did add about 18,000 new renters from 2007-2014. The next bracket up added almost 20,000 renters, and the percentage that is highly burdened, spending at least 50 percent of their income on rent, more than doubled. I wrote about this not long ago, how rent has increased in some of the city's poorest neighborhoods. In some, it hasn't gone up that much, but income has plummeted. And there are limits to how far the market can adjust—how far it can push the rent floor to meet declining incomes.

"There's a fixed cost to renting a property, to owning it and managing it," Smith says. "You're not going to see rents really go down a ton, because landlords just don't have the ability to reduce the rents, necessarily, to meet the ability of the tenants to pay. What you're seeing in the city is areas that have a lot of the low-cost housing, even if it's not affordable per se, there's also lots of households with low incomes."

Smith says the way to improve affordability in these areas is not to build more housing. He says, "It's probably supporting incomes in some way, either vouchers or some sort of subsidy on the income side of things. Those are the most affordable areas, if you're just looking at how much they cost. It's just the gap between the incomes and the rents needs to be made up somehow."