If you've read much about the housing crisis over the past couple years, you've probably come across articles that associate foreclosures and crime. It makes sense: empty homes are good places to commit crime.

The empty buildings are magnets for gang activity, depressing the value of nearby properties. Drug abuse violations and burglaries are the most common crimes taking place in abandoned properties, police report. In Austin, burglaries and illegal drug use make up 74 percent of the 66 incidents reported in the past three months. In Englewood, those crimes were 58 percent of the 85 reported cases of illegal activity. In West Englewood, drugs and burglaries constituted 43 percent of 78 incidents.

“Vacant homes create so many risks to a neighborhood,” said Charles Brown, a retired Chicago police officer living in Englewood. “Murders — we’ve found people dead in them. Attempted murder, rape, all kinds of things. They catch on fire and burn up the house next door — firemen get hurt.”

On the other hand, while foreclosed homes may be convenient places to commit crimes or hide evidence, do foreclosures actually increase or encourage crime? They may change where people choose to commit crimes—which is obviously terrible for the people who live among them—but it presumes there would be more murderers but for the lack of abandoned houses. Emily Badger takes a look at a study out of Indiana, which concludes that no, they don't:

But new research concludes that one of these fears may be only just that: there has been no direct association nationally between the housing crisis and serious crime. The new study, conducted by Professor William Alex Pridemore and doctoral student Roderick Jones at Indiana University Bloomington, counters theories and headlines (often repeated by police officials) that criminals have rushed into neighborhoods as foreclosed families have moved out.

[snip]

Pridemore and Jones controlled for the crime rates in each of these cities prior to the housing bust, as well as for a number of other variables often associated with crime, including local poverty rates, population density and unemployment rates. Their findings also contradict some neighborhood-level research that has been conducted on this same question, much of which theorized that the housing crisis had depleted the capacity of communities to respond to crime, as well as the financial ability of police departments to fight it.

In the wake of the housing crisis, research on this topic is rolling out. One recent study from researchers at UT-Austin and Virginia Tech specifically examined Chicago community areas from 2002-2009 (relying heavily on data from the Woodstock Institute), and tried to separate correlation, which is substantial in this case, from causation: "After accounting for simultaneity and time-variant and time-invariant community characteristics, the rise of recent home foreclosures has no independent effect on community crime rates. Rather, crime and foreclosures are explained by a common set of factors." It's a symptom, not a cause, of familiar old Chicago problems:

As for inequities in lending, research clearly demonstrates that predatory lending practices, such as large pre-payment penalties, balloon payments, and hefty late payment fees, are more likely targeted at poor minority communities, even after controlling for relevant factors such as borrower income and property characteristics and location…. Similar to our discussion of policing, communities differ in the extent to which they are subject to predatory and subprime lending practices, and therefore foreclosures, because they lack the political influence necessary to thwart such practices.

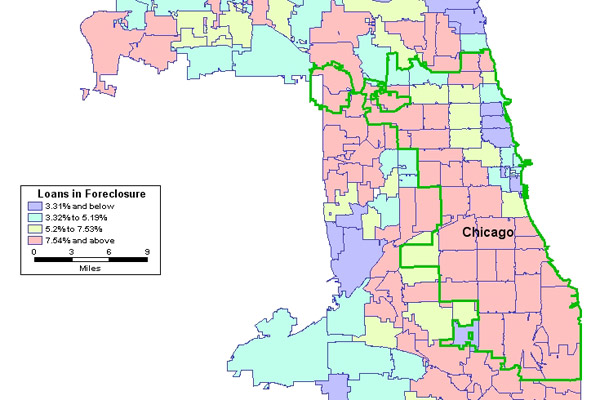

Neighborhoods with high crime are likely to suffer from waves of foreclosures because of a common foundation of poverty, and the most recent foreclosure map indicates that foreclosures in the city follow familiar patterns:

Other recent research has suggested that foreclosures actually do lead to increases in crime, but the effects are most noticable in low-crime areas.