Potential changes to America’s health care system are moving fast. Early this month House Republicans released the American Health Care Act, which lays out changes to health care policy as part of their promise to "repeal and replace" the Affordable Care Act, also known as Obamacare. On Monday, the Congressional Budget Office released its analysis of the impacts of the legislation. Last week, even without a CBO score, the bill passed out of two House committees, and yesterday it cleared a key hurdle in the House’s budget committee.

The bill could still change substantially before it's voted into law, and it faces significant opposition from both sides—as well as public opinion polls that put Republicans in a bind—but based on what's been proposed already, how would it affect our local health care system?

Trends in Cook County and Illinois don't diverge far from predicted national trends —rather, the local question is about who will be uniquely affected, especially given the constraints of the state budget. In Cook, people with lower incomes, especially the elderly, have the most to lose if the proposed legislation is passed into law.

Read on to find the major ways health care could change.

1. We would go "backward" on getting people insured

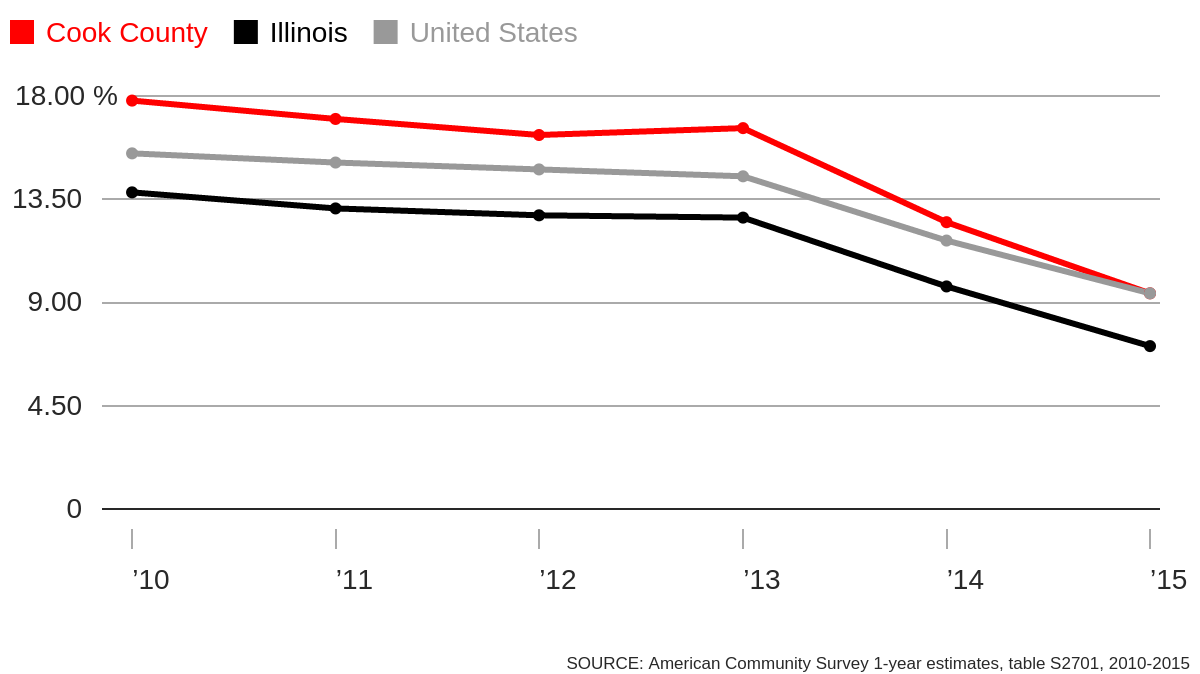

From 2010, when the Affordable Care Act was passed, to 2015, the last year for which American Community Survey data is available, the estimated percentage of people living in Cook County without insurance was cut in half. “We are at historically low rates of people who don’t have insurance,” John Jay Shannon, CEO of the Cook County Health & Hospitals System says. “What’s being proposed would make us go backward.”

Percent of all people without insurance fell

People who gained access to insurance coverage in the Chicago area over the last few years due to Obamacare are most vulnerable to losing it with the proposed changes to health care policy.

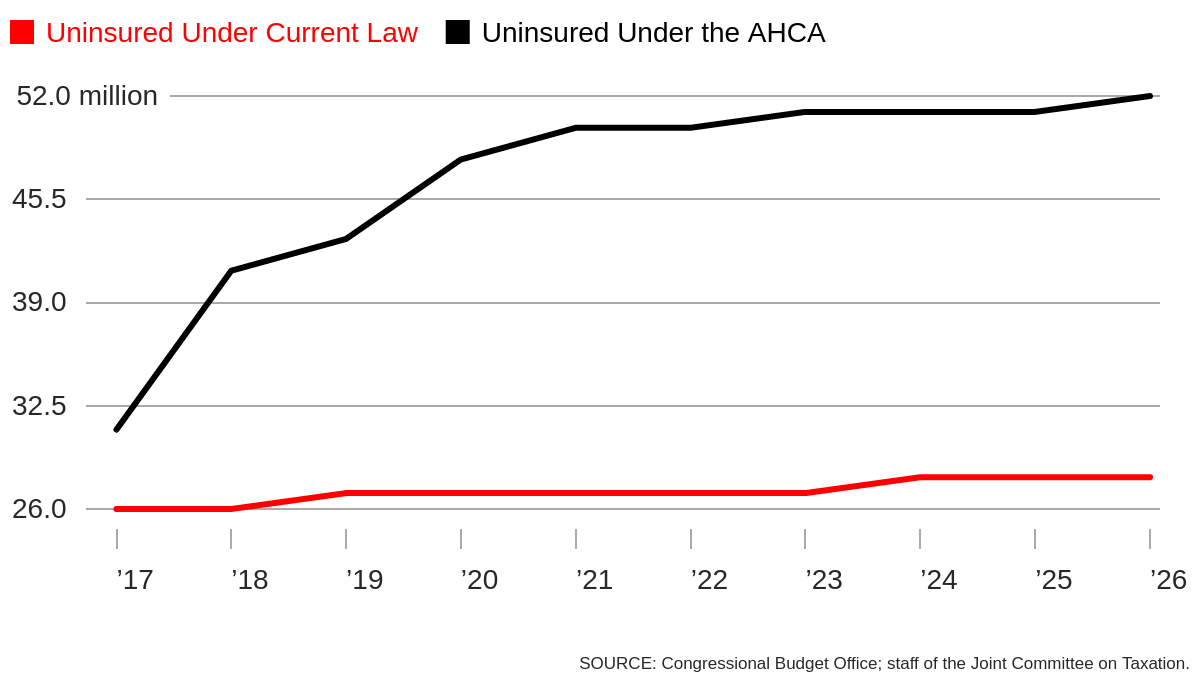

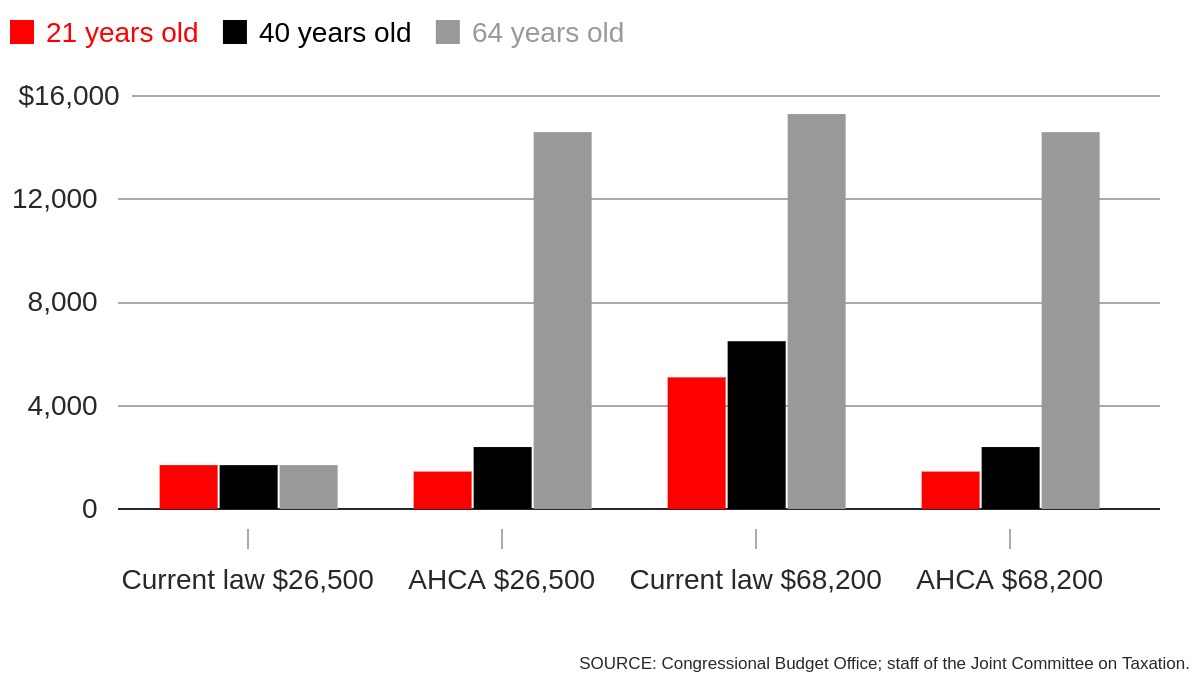

According to the CBO analysis of the proposed health care bill, by 2026, an estimated 52 million people nationwide (roughly 19 percent of the “nonelderly,” or people under 65) would be uninsured—24 million more than would be uninsured under current law.

Uninsured people younger than 65, current law vs. AHCA

2. It's easy for new Medicaid enrollees to get dropped

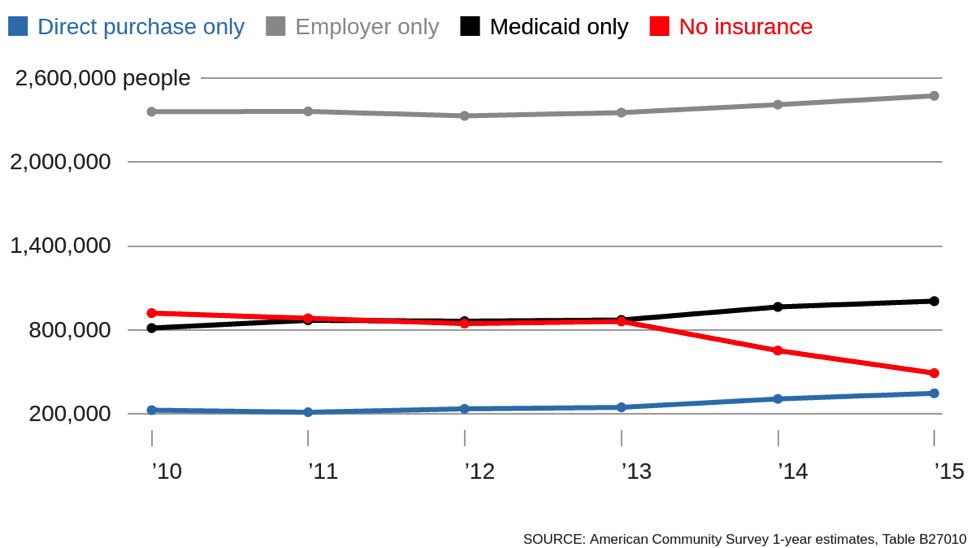

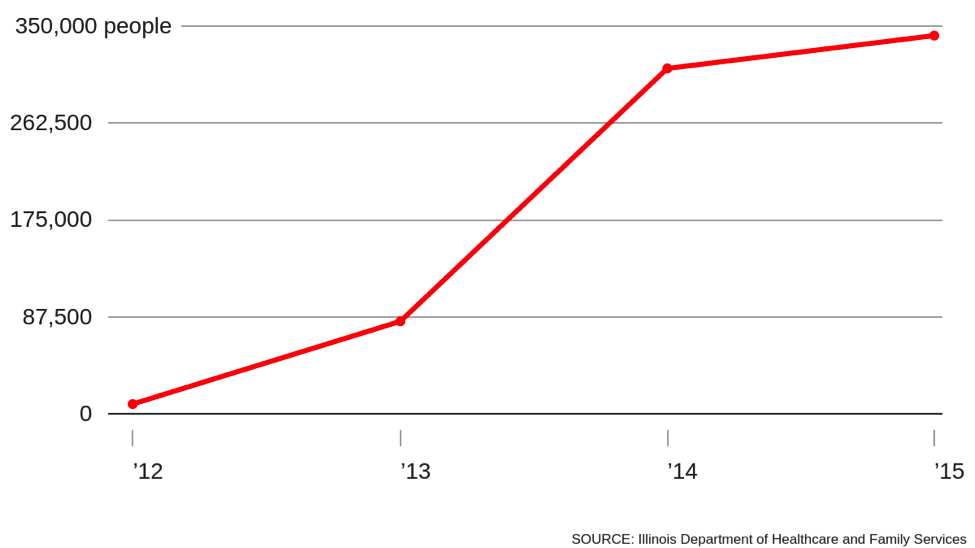

Many of those affected are new enrollees in Medicaid, the government insurance program for low-income people. In Cook County, Medicaid has seen the largest growth compared with other types of insurance. The ACA included federal funding for a Medicaid expansion by loosening eligibility rules, which Illinois gladly accepted, giving around 350,000 people living in Cook County insurance.

The number of Medicaid enrollees rose as the number of uninsured fell

“Prior to the Medicaid expansion you had to be low income—and a mother, and disabled” to receive support, says Megan Doerr of CommunityHealth, the largest free clinic in the nation. After the ACA, she says, a person only needs to have a low-enough income to enroll—about $16,643 for an individual or $33,948 for a family of four.

This was a big deal for CommunityHealth, which provides free health care for uninsured people in Chicago. With the expansion of Medicaid, as well as other policies that made insurance more affordable, the organization was able to help some of its patients transition to other providers. The organization saw the number of its medical patients decrease by nearly 22 percent from its high in 2013 to 2016, helping to reduce the burden on their volunteer doctors, who were often overbooked.

The AHCA allows federal funding for new Medicaid enrollees under the old rules until 2020. After that, if a person became ineligible (under the new rules) for more than one month, the federal government would no longer pay for their care.

“The impact would be dire,” Shannon says, adding that Illinois likely cannot afford expanded Medicaid coverage without the federal help—in which case the state will likely end the loosened eligibility rules.

Medicaid expansion in Cook County

3. Older people with low incomes would face higher insurance costs

New Medicaid saw the largest total jump in Cook County, but the group that grew most percentage-wise was direct purchase insurance—just over 40 percent from 2013 to 2015, according to an analysis of American Community Survey estimates from 2010-2015.

Two key parts of the ACA factor into this: The law requires people to have health insurance or pay tax penalties, and it also offers tax credits to help make the premiums affordable. Among those directly purchasing their own insurance, 144,418 in Cook County used the government health insurance marketplace as of 2017, according to the federal government. About 73 percent of them qualified for some kind of tax credit, which are based on a person’s income and the price of a mid-level plan on the marketplace, ensuring that premium costs do not exceed a certain percentage of income.

But under the AHCA, people instead get a fixed tax credit based mostly on age, rather than income. The older you are, the larger your credit. Second, people with higher incomes (previously ineligible under ACA) are now eligible for credits. Under this scheme, people earning lower-incomes would see less help in paying for their insurance.

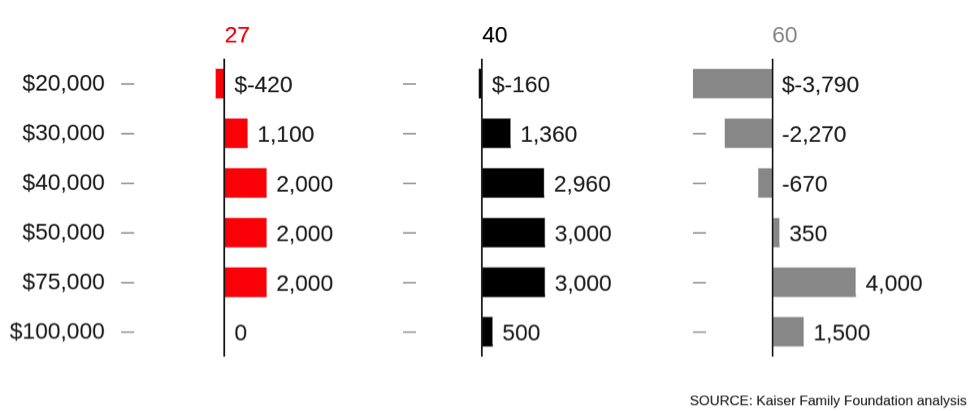

The Kaiser Family Foundation calculated tax credit amounts for different groups of people under the ACA and AHCA for 2020, the year in which the AHCA credits would take effect.

Estimated change in tax credits available due to AHCA in Cook County

A 60-year-old earning $20,000 a year would receive nearly $3,800 less in credits under the proposed legislation. A 60-year-old making $75,000 a year, previously ineligible for a credit, would get $4,000 toward their insurance premiums.

Insurers have always charged older people with higher premiums, but due to the ACA, they cannot set premium prices for one age group at more than three times the cost of the least expensive age group. (Looking at 2017 silver-level plans available in Cook County on the Marketplace, premiums for a 60-year-old are about 2.71 times those of someone who is 21.)

The AHCA allows insurance companies to charge older people up to five times the premium of the youngest age group. “People will pay more for their health care coverage—bottom line,” according to Courtney Hedderman, Associate State Director for Advocacy, for AARP Illinois, an advocacy group for people over 50 that has voiced its opposition to the AHCA.

Premiums after tax credits: being both old and lower-income means paying more

4. Everyone will see higher deductibles

In general, under the new legislation, deductibles would go up, according to the CBO analysis. Currently, the federal government tries to make coverage more affordable by offering the same insurance plan with different deductibles, a form of what is known as cost-sharing. If you make less money, your deductible will be lower than a person with a higher income who is purchasing the same plan.

With the AHCA, this cost-sharing help goes away, so regardless of your income, you’ll be paying the same deductible.

The new plan will also eliminate a rule that requires insurance plans to pay for at least 60 percent of costs, meaning some new plans may offer very minimal coverage, possibly with low premiums and high deductibles, a type of plan often favored by younger, healthier people. The familiar tiers of Bronze, Silver, Gold, and Platinum plans on Get Covered Illinois are based on the percentage of costs that each plan pays for—AHCA will eliminate that ranking system. The CBO predicts this will make comparing plans by price more difficult for consumers when shopping for insurance.

5. Illinois won’t be able to pay Planned Parenthood for a year

There are many health care providers in Chicago, but only one is explicitly targeted under the AHCA: Planned Parenthood. Though the act doesn’t name the provider explicitly, the legislation says states cannot use federal funds to pay a “prohibited entity” that, according to the CBO analysis of the bill, would only affect Planned Parenthood. Payments to the organization would be blocked for one year.

A little over one third of Planned Parenthood's patients are on Medicaid, according to the group, and that's where the federal funds freeze will hurt the most, according to the CBO. (It also gets funding to subsidize care such as contraception, STI screenings and cancer screenings under a Nixon-era program known as Title X.)

The CBO predicts that this would limit access to contraception for some women, particularly those living in areas with few family-planning providers for low-income women. In Cook County, Planned Parenthood clinics saw almost 32 percent of female patients seeking contraception, according to a 2010 census of publicly funded clinics by the Guttmacher Institute, a research organization that studies and advocates for reproductive health access. Only Federally Qualified Health Centers saw more, nearly 42 percent of contraception patients.

“The question is, where else could they turn?” Planned Parenthood of Illinois interim CEO Linda Diamond Shapiro says. Unlike many other providers, Planned Parenthood focuses on reproductive health care, Shapiro says, stressing that clinics in Chicago offer a wide range of contraception options and the ability for patients to get contraception quickly.

6. Savings for the federal budget; Cook County and Illinois, not so much

Right now, the federal government pays for Medicaid care regardless of the health care costs and needs of any individual patient. Under the AHCA, there would be a per-person cap on the amount of Medicaid funds received by Illinois, giving the state a lump sum based on the number of insured regardless of the actual costs of care.

If Illinois doesn’t have enough money to cover Medicaid costs, both Shannon and Hedderman said there are few options. The state could limit eligibility for the program, cut the services that are covered or cut payments to health care providers.

The cuts to Medicaid payments, the move away from income-based subsidies, and the elimination of cost-sharing reductions would result in a reduction to the federal budget deficit, according to the CBO—a reduction of $337 billion over the 2017-2026 period.

In Cook County, however, the Medicaid expansion whose elimination makes up the largest chunk of the federal deficit savings has brought money into the county budget. In the last eight years, county tax money spent on the Cook County Health and Hospital System dropped from $481 million to $111.5 million, according to numbers from the system. Though some of the drop comes from improvements in things like billing, most of the drop comes from increased revenue from more patients being covered by Medicaid.

Cook County also runs a Medicaid plan, CountyCare, which last year paid $300 million to community providers—clinics, hospitals, long term care, facilities, and pharmacies. With Medicaid expansion ending and federal dollars drying up, these payments will likely shrink. For some of these providers, changes to these payments could significantly stress their budgets, Shannon says.

In February, President Donald Trump spoke about his commitment to repeal and replace the policies of his predecessor. “I have to tell you, it’s an unbelievably complex subject,” Trump said. “Nobody knew that health care could be so complicated.”

Health care policy is complex, especially for those whose access depends on many moving parts within the federal government. When the Affordable Care Act was rolled out, CommunityHealth and other community organizations helped uninsured people apply for coverage under Medicaid or purchase insurance through the online marketplaces. Many were confused about the law and how it impacted their lives.

Doerr suspects a similar dynamic if significant changes are made to health care laws. “History tells us that we are once again going to deal with a lot of confusion,” Doerr says.